Pan-African fintech company Interswitch plans to fire up its corporate venture arm again—according to CEO Mitchell Elegbe—who spoke at TechCrunch Disrupt on Wednesday.

The Nigerian founder didn’t offer much new on the Lagos-based firm’s expected IPO, but he did reveal Interswitch will revive investments in African startups.

Founded by Elegbe in 2002, Interswitch pioneered the infrastructure to digitize Nigeria’s then predominantly cash-based economy. The company now provides much of the rails for Nigeria’s online banking system that serves Africa’s largest economy and population of 200 million people. Interswitch has expanded to offer personal and business payment products in 23 Africa countries.

The fintech firm achieved unicorn status in 2019 after a $200 million equity investment by Visa gave it a $1 billion valuation.

Reviving venture investing

Interswitch, which is well beyond startup phase, launched a $10 million venture arm in 2015 that has been dormant since 2016, after it acquired Vanso—a Nigerian fintech security company.

But Interswitch will soon be back in the business of making startup bets and acquisitions, according to Elegbe. “We’ve just certified a team and the plan is to begin to make those kinds of investments again.”

He offered a glimpse into the new fund’s focus. “This time around we want to make financial investments and also leverage the network that Interswitch has and put that at the disposal of these companies,” Elegbe told TechCrunch.

“We’ll be very selective in the companies we invest in. They should be companies that Interswitch clearly as an entity can add value to. They should be companies that help accelerate growth by the virtue of what we do and the customers that we have,” he said.

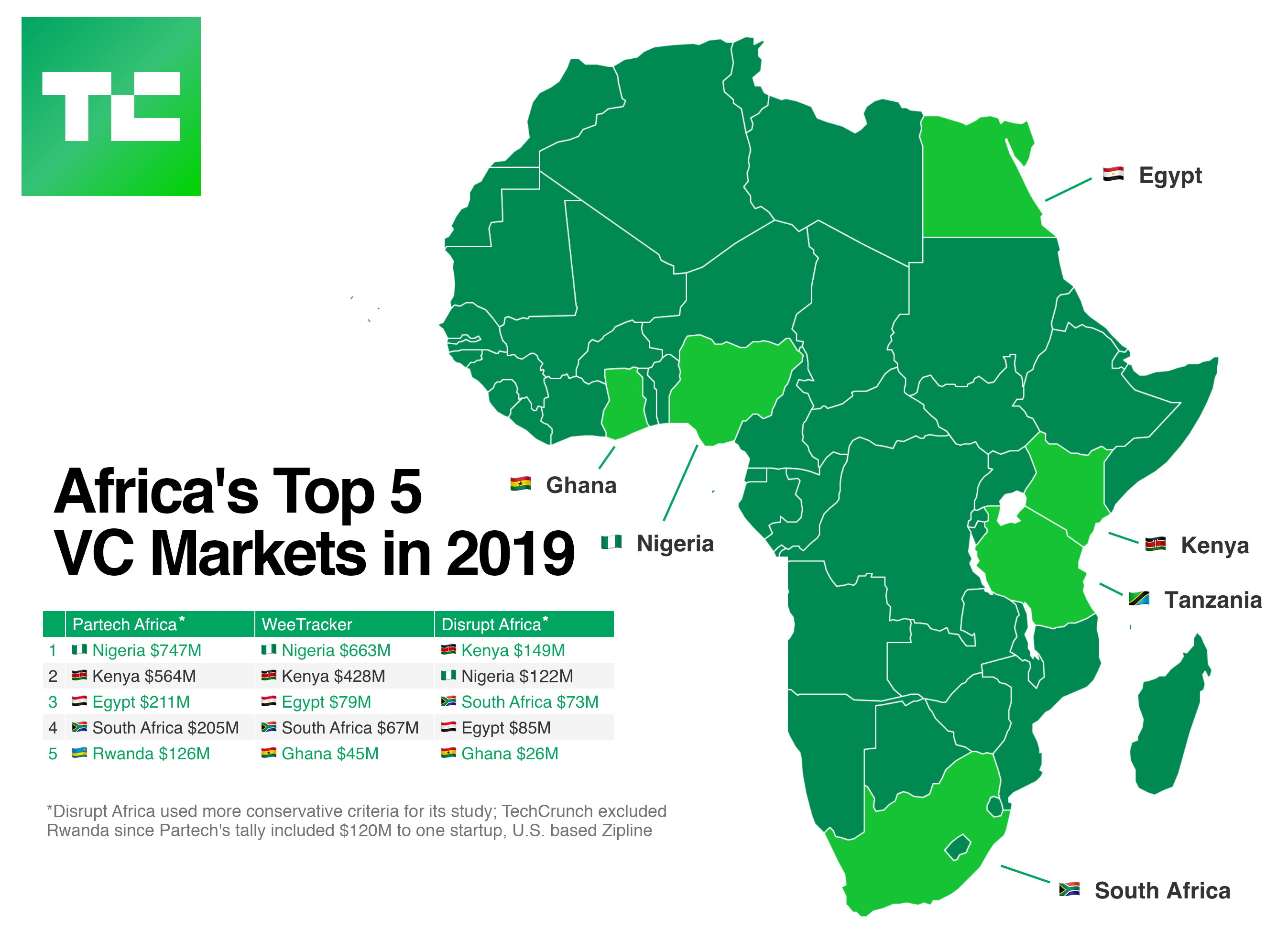

Recent venture events in African tech have likely pressed Interswitch to get back in the investing arena. As an ecosystem, VC on the continent has increased (roughly) by a factor of four over last five years, to around $2 billion in 2019. But most of that has come from single-entity investment funds, while corporate venture funding (and tech M&A activity) has remained light. That’s shifted over the last several months and the entire uptick has occurred in African fintech around entities that could be viewed as Interswitch competitors.

In July, Dubai’s Network International acquired Kenya -based payment mobile payment processing company DPO for $288 million. Shortly after the acquisition, DPO’s CEO Eran Feinstein said the company would pursue more African acquisitions on its own. In June, another mobile-money payment processor, MFS Africa, acquired digital finance company Beyonic. And in August, South Africa’s Standard Bank—Africa’s largest by assets and lending—acquired a stake in fintech security firm TradeSafe.

Since the rise of Safaricom’s dominant M-Pesa mobile money product in Kenya, fintech in Africa has become infinitely larger and more competitive. The sector has hundreds of startups and now receives nearly 50% of all VC investment on the continent.

The opportunity investors and founders are chasing is bringing Africa’s large unbanked population and underbanked consumers and SMEs online. Roughly 66% of Sub-Saharan Africa’s 1 billion people don’t have a bank account, according to World Bank data, and mobile-based finance platforms have presented the best use-cases to shift that across the region.

Interswitch has established itself as a leader in the Africa’s digital finance race. But it’s hard to envision how it can maintain or extend that role without an active venture arm that invests in and acquires innovative, young fintech startups.

No news on IPO

Elegbe had less to offer on Interswitch’s long-anticipated IPO. Asked if the company still planned to list publicly, he offered up a non-answer answer. “At this point in time we’re focused on growing the business and creating value for our customers and that is the our primary focus.”

When pressed “yes or no” on whether an IPO was still a possibility Elegbe confirmed it was. “We have private equity investors and at some point in the life of the business they want exits.” he said. “When it is time for them to exit there are various options on the table and an IPO is an option.”

There’s been talk of an Interswitch IPO for years. In 2016, Elegbe told TechCrunch a dual-listing on the Lagos and London Stock Exchanges was possible. Then word came through other Interswitch channels that it was delayed due to recession and currency volatility in Nigeria in 2017. In November 2019, a source with knowledge of the situation told TechCrunch on background, “an IPO is still very much in the cards; likely sometime in the first half of 2020.” Then came the Covid-19 crisis and the accompanying global economic slump, which may have delayed Interswitch’s IPO plans yet again.

If and when the company goes public, it would be a major event for Nigerian and African fintech. No VC backed fintech firm on the continent has listed globally. Exits for Interswitch’s investors would likely attract to Nigeria and broader Africa more VC from major funds—many of whom remain on the fence about startup opportunities on the continent.

Focus on Africa

On global product expansion, Interswitch plans to maintain an African focus for now, Elegbe explained. “There are enough opportunities for Interswitch on the continent. We’d like to be in as many African countries as possible…and position Interswitch as the (financial) gateway to the continent,” he said.

Elegbe explained the company would continue to work through alliances with major financial services firms to open up global financial access for its African client base. In August 2019, Interswitch launched a partnership that allows its Verve cardholders to make payments on Discover’s global network.

CEO Mitchell Elegbe concluded his Disrupt session with some perspective on balancing the stigmas and possibilities of doing business in Nigeria. Over recent years the country has shifted to become an unofficial hub for big tech expansion, VC investment, and startup formation in Africa. But Nigeria continues to have a difficult operating environment with regard to infrastructure and is often associated with political corruption and instability in its Northeast region due to the Boko Haram insurgency.

“Nigeria has a very large population and a very large market. We have lots of challenges that need to be solved, but it makes sense to me that lots of money is finding its way to Nigeria because the opportunity is there,” he said.

Elegbe’s advice to tech investors considering the country, “Don’t take a short-termist view. There are good people on the ground doing fantastic work—honest people who want to make impact. You need to seek those people out.”