Americans are saddled with $1.2 trillion in auto loans, according to data collected by the Federal Reserve. And while that debt can be refinanced, even U.S. car owners who know it’s an option face a complicated task.

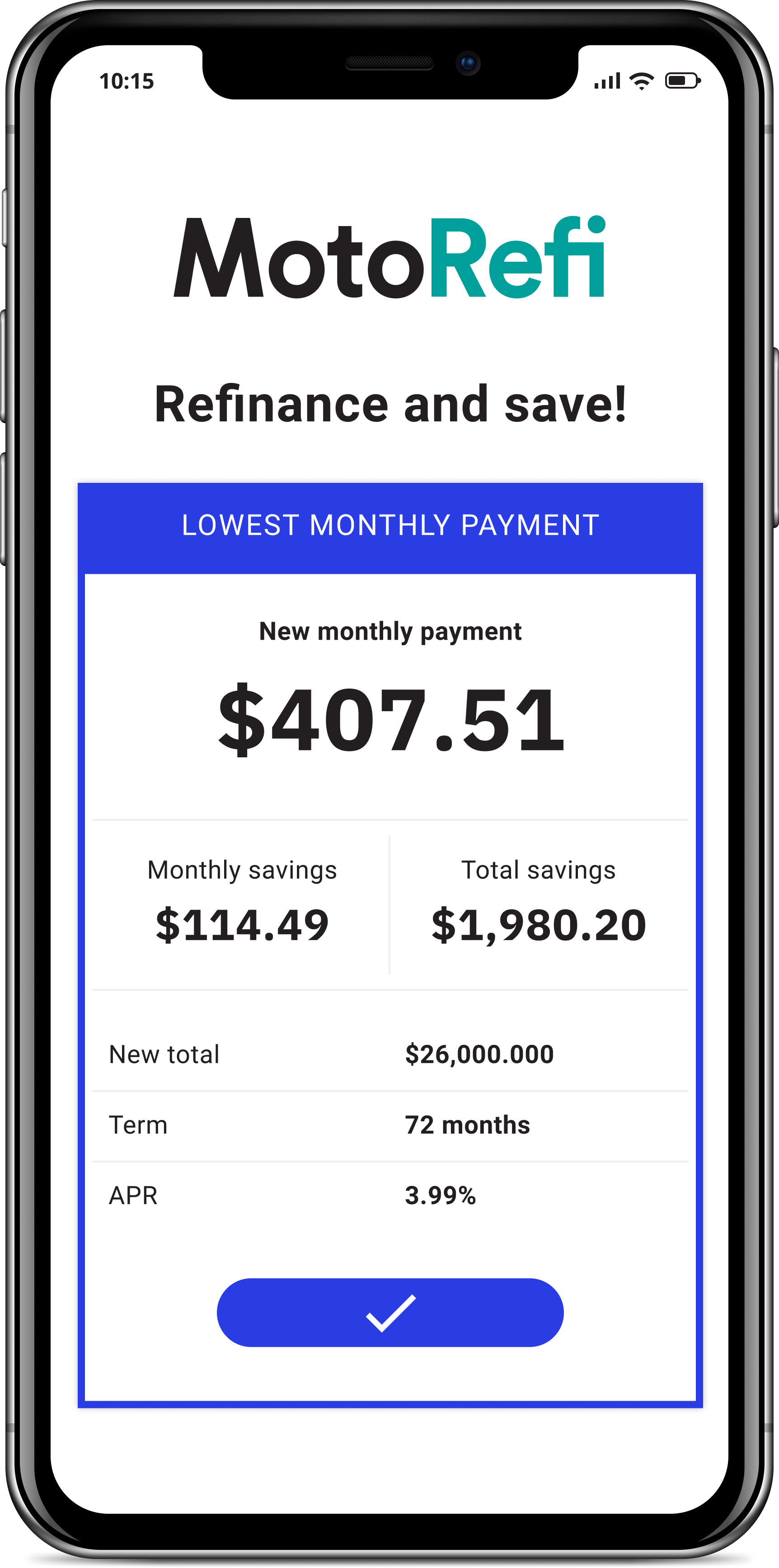

MotoRefi, a new fintech startup that was born out of QED Investors in 2017, says it has developed an auto refinancing platform that handles the entire process, from rooting out the best rates to paying off the old lender and re-titling the vehicle.

Now, the company is preparing to scale up and bring its platform to the masses, with $8.6 million in capital raised in a Series A funding round co-led by Accomplice and Link Ventures. Motley Fool Ventures, CMFG Ventures (part of CUNA Mutual Group) and Gaingels also participated in the round. The round follows $4.7 million in seed funding that MotoRefi announced in March 2019.

MotoRefi is also gaining two new board members, Rob Chaplinsky, managing director of Link Ventures, and Rachel Holt, former Uber executive and co-founder of a new VC firm, Construct Capital.

Auto loan debt is the same as student loan debt in the U.S., said MotoRefi CEO Kevin Bennett. And yet the majority of car owners don’t know that refinancing their auto loan is even an option, he added. A 2017 Harris Poll found that 47% of Americans were aware they could refinance their auto loan.

“People shop their home loans, while most just get their auto loans from the dealership where they bought their car, so their rates are artificially high,” Bennett said in a recent interview. “Meanwhile, credit unions can be great for auto loans but they might not have the tools to reach consumers.”

That’s where MotoRefi hopes to step in. Bennett said the MotoRefi platform can save customers an average of $100 per month on their car payments.

Holt, who was an early investor in MotoRefi, said during her time at Uber she saw firsthand the amount of auto loans drivers were carrying. Dealerships aren’t making money on selling cars, they’re making it on financing, Holt said. “I saw this problem and so I was looking out for startups trying to solve this problem,” she added.

The U.S. auto refinancing market is about $40 billion, according to TransUnion. But that market could be two to three times that size, according to data shared at TransUnion Financial Services Summit. It’s an opportunity that has prompted companies like Lending Tree to launch auto refinancing products.

MotoRefi is already scaling up by adding new lenders and partners, according to Bennett. The new funding will be used to hire more employees and invest in its technology platform.

The startup also launched in January separate pilot programs with Progressive and Chime. Under these pilots, Progressive and Chime will directly offer refinance options to their customers instead of going through an affiliate program such as Credit Karma — a company backed by QED Investors — or LendingTree.